IAS 24 | RELATED PARTY DISCLOSURES

Written by: Sohail Tahir

IAS 24 explains and requires the disclosures about transactions (activities) take place during the financial year. It also requires to disclose the outstanding balances of related parties at the reporting date. Furthermore, it sets out the disclosures about compensation of management personnel.

Need of IAS 24

Related party disclosures draw attention towards the possibility of misstatement in financial statements of the entity due to existence of related party(ies).

Generally, in small and medium sized entities, related parties are difficult to identify due to lack of formal procedures for identification of related parties and related party transactions. While developing and understanding the procedures to identify relate party transactions, one must understand who are related parties to the entity?

RELATED PARTIES

A related party may be a person, association of persons, company or any other entity that is related to the reporting entity (‘a reporting entity is the one who is going to prepare its financial statements’).

Condition 1

If a person or any of his close relative

- controls or jointly controls the reporting entity; or

- is in a position to influence the reporting entity significantly; or

- is a part of key management of the reporting entity, or of a parent of the reporting entity

then that person or any of his close relative are considered as related party(ies) of the reporting entity.

Example

Mr. A is a Chief Executive Officer of New Cars (Private) Limited (reporting entity). His sister Miss. B is a business women and is running a boutique.

As Mr. A is a Chief Executive Officer of New Cars (Private) Limited, which clearly shows that he is in a position to control the entity and also a part of key management personnel. Hence Mr. A and News Cars (Private) Limited are related parties in the light of IAS – 24.

Miss B is a close relative of Mr. A and she may indirectly be in a position to influence the reporting entity. Hence, in the light of provisions of IAS-24, Miss B and New Cars (Private) Limited are considered as related parties.

Condition 2

If an entity and the reporting entity are part / members of the same group, then that entity and reporting entity are considered as related parties.

Example

New Cars (Private) Limited (reporting entity) is a subsidiary of Big Cars Limited, who is also a parent company of Fine Trucks (Private) Limited.

As all three companies are part of one group, hence, Big Cars Limited and Fine Trucks (Private) Limited, both are related parties to New Cars (Private) Limited.

Condition 3

If an entity is an associate or joint venture of the reporting entity, then that entity and reporting entity are considered as related parties.

Example

New Cars (Private) Limited (reporting entity) and Fine Cars (Private) Limited entered into a Joint Venture i.e. New Fine JV for the purpose of manufacturing 1,000 cars on special request of Federal Government.

New Fine JV is related party to New Cars (Private) Limited.

Condition 4

If an entity and the reporting entity are joint venture of same third party, then that entity and reporting entity are considered as related parties.

Example

New Cars (Private) Limited and Fine Cars (Private) Limited entered into a Joint Venture i.e. New Fine JV (reporting entity) for the purpose of manufacturing 1,000 cars on special request of Federal Government.

For Armed Forces, New Cars (Private) Limited also went into a Joint Venture with Excellent Cars (Private) Limited by the name of N & E Cars JV for the purpose of manufacturing 500 special purpose jeeps.

N & E Cars JV and Fine JV are related parties of each other

Condition 5

If one entity is a joint venture of any third entity and the second entity is an associate of the third entity, then first and second parties are considered as related parties.

Example

New Cars (Private) Limited and Fine Cars (Private) Limited entered into a Joint Venture i.e. New Fine JV (reporting entity) for the purpose of manufacturing 1,000 cars on special request of Federal Government.

Mr. A who is director and shareholders of New Cars (Private) also owns a cars spare parts business as a sole proprietor by the name of Car Care.

As Fine JV is a joint venture of New Cars (Private) Limited and Car care is an associated business of New Cars Private Limited, hence, Fine JV and Car care are considered as related parties.

Condition 6

Entity A and Entity B are considered as related parties of each other if:

- Entity A is a reporting entity; and

- Entity B is a post-employment defined benefit plan for the employees of, Entity A, or of entity related to Entity A.

If reporting entity itself a post-employment defined benefit plan, then reporting entity and employer(s) contributing in the benefit plan are considered as related parties.

Example

New Cars (Private) Limited created gratuity fund for the welfare of its employees by the name of New Cars Employees Gratuity Fund. The fund is registered and is recognized by the Tax Department.

New Cars (Private) Limited and New Cars Employees Gratuity Fund are related parties.

In case more than one employer is contributing in the fund, all the employers are considered as related party to the defined benefit plan entity.

Condition 7

If reporting entity is controlled by person individually or jointly then all the controlling parties are considered as related parties.

Example

New Cars (Private) Limited (NCPL) is involved in manufacturing of cars and trucks since 2010. Mr. A and Mr. B are equal shareholders in NCPL.

Mr. A and Mr. B, both are related parties of NCPL.

NON-RELATED PARTIES

Following parties are not considered as related parties to each other:

- Two entities simply by virtue of common directorship or key management involvement

- Two joint venturers who share joint control over a joint venture

- Finance providers, trade unions and government agencies that do not control individually or jointly, or in a position to significantly influence the reporting entity, as they are involved in a normal dealing way

- Customers and other stakeholders with whom an entity transacts in a normal dealing way

RELATED PARTY TRANSACTIONS

Activities or transactions, regardless of involvement of cash, occurred or resources and services are transferred or rendered between two related parties, are known as related party transactions.

If terms of transaction are substantial, then a statement may be made that related party transactions are made on the terms equivalent to those prevail in an arm’s length transaction.

RELATED PARTY DISCLOSURES

In case of existence of related party transactions, entity shall disclose the following in addition to the disclosure of key management personnel compensation:

- Nature of the related party relationship

- Amount of related party transactions

- Outstanding balances and commitments

- Terms and conditions of transactions

- Provision for doubtful debts related to the outstanding balances

- Bad debts in respect of related party balances recognized during the year

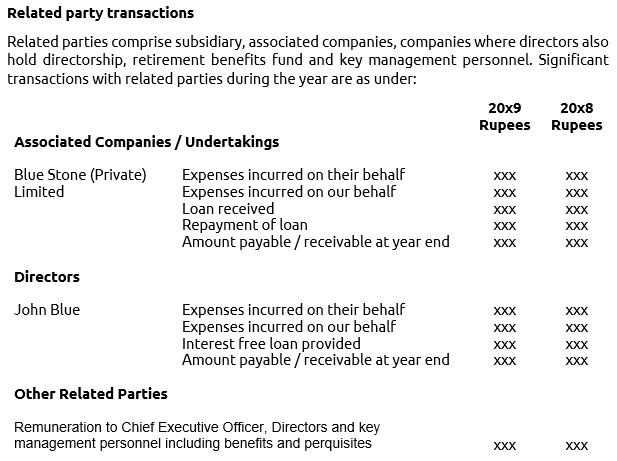

For the purpose of basic understanding, extracts of related party disclosure are mentioned below:

IMPORTANT INFORMATION

Entity must disclose the name of its parent (if any) regardless of existence of transaction with its parent. In case of multiple controllers, name of ultimate controller must be disclosed.

If neither the parent nor the ultimate controller produces financial statements available for public use, then the name of next most senior parent must be disclosed.

If one entity of the group obtains management personnel services from the other entity of the same group (management entity), then the entity is not required to disclose the compensation paid or payable to management personnel. Alternatively, the entity shall disclose the amount as incurred by the entity on our behalf. Any payment to management entity shall decrease the amount of incurred by entity on our behalf. However, the amounts must be disclosed separately.